Composites industry GBI contracted faster in July

The GBI: Composites maintains its consistent downward trend for the fifth month in a row.

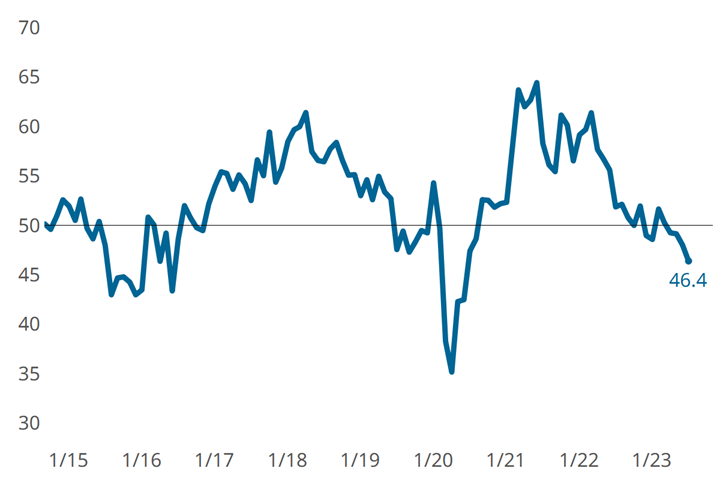

Index consistency. GBI: Composites Fabricating in July was down 1.6 points from June. Photo Credit, all images: Gardner Business Intelligence

The Gardner Business Index (GBI): Composites Fabricating closed July at 46.4, down 1.6 points from June. If there is comfort in consistency and predictability (not to be confused with stability), the Composites Fabricating index has a lot to offer.

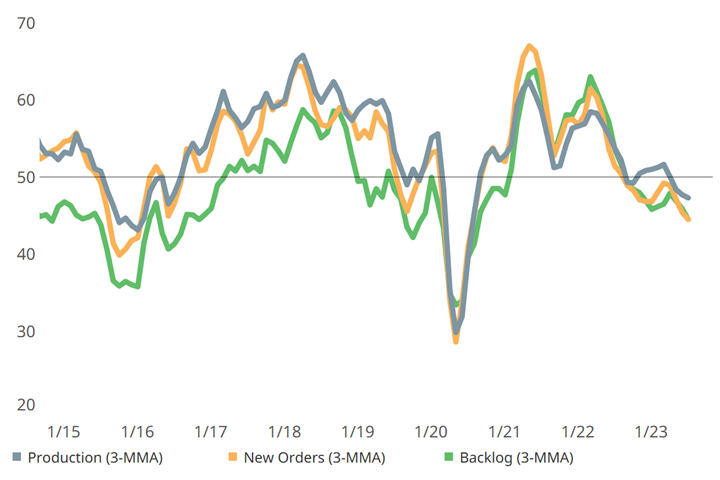

Most index components have been declining and, in some cases, “contracting,” since March/April 2023. The three closely linked manufacturing GBI components, new orders, production and backlog, contracted faster again in July. Exports contracted at a steady rate, continuing this same level of activity since April 2022.

Employment and supplier deliveries tracked similarly again, both remaining in expansion and lengthening, respectively — though employment just barely. Employment is threatening to go “flat,” and may even contract in the near future.

Future business, a sentiment/outlook metric that is not part of the GBI calculation but related to it, offers evidence of optimism in a July read that reports more people think business will be up (versus down) in the next 12 months.

Components contracting. Three closely linked manufacturing GBI components, new orders, production and backlog, contracted faster again in July. (This graph is moving on a three-month moving average.)

Related Content

-

Composites Fabricating Index loses ground in April amid tariff uncertainty

Latest reading of 47.3 is fueled by a drop in new orders as markets react to quick changes in trade policy.

-

Composites industry gained back some ground in December

The GBI: Composites Fabricating contracted a little more slowly in December, landing between August and September 2023 values.

-

Composites industry GBI stayed the course in February

The GBI: Composites Fabricating contracted in February to the same degree as January, maintaining its position in a contraction zone.