Selling your business, Part 1: The best price with the best deal

Adrian Williams, co-founder and managing director of Future Materials Group (Cambridge, UK), begins a two-part advisory for owners of composites manufacturing businesses interested in placing their companies on the market.

Adrian Williams is co-founder and managing director of Future Materials Group (Cambridge, UK), an independent strategic advisory firm. Its services include growth strategies, mergers and acquisitions, strategic partnerships and growth capital.

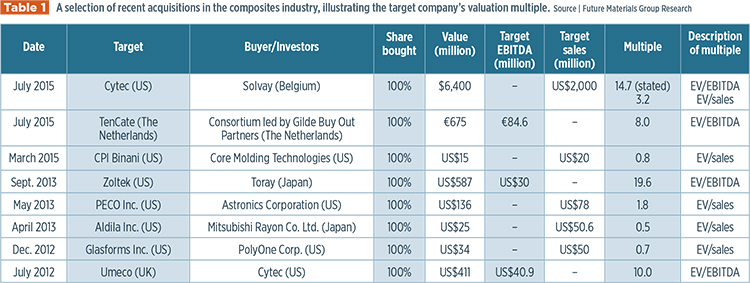

Table 1: A selection of recent acquisitions in the composites industry, illustrating the target company’s valuation multiple. Source: Future Materials Group Research

Investors throughout the world have a positive perception of the composites industry. They see growth opportunities across many sectors – aerospace, automotive, wind energy, pressure vessels, oil and gas, rail and mass transport. Overall, margins and return on investment are attractive, especially compared to many other manufacturing segments. And they like the choice that the diverse composites business models offer, with different mixes of capital and margin intensities throughout the supply chain, to match their investment strategies and portfolios.

Relatively young and fragmented, the industry attracts particular attention from three discrete investment communities:

- Mid-market financial investors who seek strong growth opportunities in the manufacturing sector;

- Trade buyers who want to diversify into a higher growth market;

- Industry players looking to expand into new markets, broaden their product portfolio or consolidate.

As attractive as they might be, owners and shareholders who are looking to sell to one of these groups must not neglect the following all-important tasks of preparation if they are to be successful. Planning and timing are key. Toward those objectives, we have developed a comprehensive five-step process:

- Effective positioning and presentation;

- Intelligent research;

- Identification, selection and approach to the right buyers;

- Creation and management of a competitive process;

- Avoidance of legal, regulatory and tax pitfalls.

Throughout, there are always requirements for diligence with your planning, awareness of your timing of each action, and an overall approach that concentrates on the end result.

1. Effective positioning and presentation

Define your goals. First, clarify your commercial and your personal objectives. Have you decided on a timeframe? It is rigid or flexible? What about succession planning? Will your children take over the enterprise, or the present management team, or new blood, or a mixture? Will you really leave entirely or will you seek further involvement, possibly over a defined period?

This scenario assumes there’s one owner, or a majority shareholding, with others willing and able to tag along with the sale. But most often, businesses have a raft of active, and not-so-active, shareholders, with a distinct lack of alignment between their wishes, hopes and ideas. A lack of orientation makes the business difficult to sell, and certainly hinders external investment.

When a business starts up, the funding — from friends, angels and other sources — and the shareholding and shareholder agreements are often informal, varying in their terms and conditions, and may include other considerations, promises and assurances. The priority at start-up is to get the cash, from wherever and whoever shows a willingness to invest. At FMG, we find that the result is a not unusual mix of investor goals and personal agendas, and a resulting lack of commonality.

Shareholder alignment is essential but can be a bit like herding cats. Nevertheless, it must be dealt with at the earliest opportunity and in place before any exit option is considered or planned. Then a number of questions must be answered:

Who is your likely buyer? For most medium-sized businesses, a buyer comes in two guises:

- Financial investor. Usually a private equity group or potentially a ‘family office,’ their fundamental interest is the financial return on their investment. They look for opportunities where the commercial concept is proven and scaling the business involves developing sales and marketing channels. Any large investment in capacity makes the acquisition less attractive for them.

- A strategic or trade buyer. Typically a large business buying up a smaller business, a trade buyer expects to see strong synergy benefits for their business, as well as the all-important return on investment. A large trade buyer often brings an operational capability that can add and efficiently manage capacity.

Alternatively, if you’re considering an initial public offering (IPO), you need a very aggressive growth story and/or a very compelling investment hypothesis to appeal to potential shareholders. You must demonstrate a proven commercial concept, the need and opportunity to scale the business, and that the scale-up opportunity is significant.

A financial investor typically wants to partner with existing management over an agreed timeframe. With a trade buyer, there might be an agreement that you continue in management, but that’s less certain. (The IPO route is expensive and can be lengthy, but it is possible to maintain control of the business.)

What is your company’s actual worth? This is the time to formulate some idea of the company’s value. Table 1 (at left), for example, lists recent and in-progress deals and the value of the target firms. The composites industry is broad in scope, and so can be the valuations, but there are commonalities. Multiples of revenues, profits, gross profits and more can all be explored and tested with the help of advisers who have up-to-date knowledge of the present and future market indicators and the likely buyers.

What will your buyer actually be buying? A differentiated and compelling proposition is the most valuable sales tool you have to sell your products. Define exactly what your business is: its technology, its markets and its customers. Demonstrate a complete and thorough understanding of your target markets, and why you are competitive in those sectors. Be prepared to show a buyer the realistic growth opportunities for the business — validated, assessed and with evidence. If your assessment forecasts growth that exceeds the expected market growth, then you need a strong argument outlining why your firm will perform better.

Fast growth is limited. In manufacturing, you are part of a supply chain. Investment in people, facilities and equipment is required, and it takes time for new composites technologies, materials and processes to prove their utility and quality, as well as the robustness of their delivery and consistency. The growth rates and profitability levels and, therefore, your return on investment, will be more modest than if you were in the IT sector, where firms can spring up and attain high valuations in months. On the plus side, if you have established a strong niche, there is a much-reduced risk of the business failing because the customers who use your products have fewer options. As a result, you can command a higher valuation.

Where do you sit in the value chain? Your position here, and the dynamics of your supply chain, are a core piece of your business model. We see numerous business models with serious flaws because the company does not fully understand how its supply chain works, and its position in that value flow.

2. Intelligent research

Develop a roadmap. A potential buyer needs to know more than your company. Who are your customers, your competitors and what is your geographic reach? Analyze where the business is today to create a picture of where it could be in the future, and what financing will be needed to enable the transition. A technology/product development roadmap is a good tool here. It must detail the point in time you are expecting to launch a new product and assess the business environment for that product at that time. If there is potential for the business to expand geographically, look at the regulatory environment for your product, geography-by-geography, and show its effect on your competitiveness and value proposition. When you project the company’s future position, outline your market growth, market share, geographic expansion, sales volume and capacities. To demonstrate your company’s potential to a buyer, we suggest you create a detailed plan for the first three years, followed by a trajectory that shows where the business could be in five years. Once you have a roadmap, identify key milestones that will drive the business over that time period. You can then relate your financial needs to these milestones.

This roadmap, with milestones and financing needs, alongside a very clear value proposition and supporting data, is a very effective way to communicate your business plan to potential buyers. Ideally, you also should be able to distill your three-to-five year plan into a couple of paragraphs. We rarely see this done well, but an external adviser, like FMG, can add valuable insight here.

How much must I invest to get that sale?

When you have decided to sell, you need to agree that you will go ahead with a properly funded and professionally executed plan and engagement with buyers (to be covered in Part 2 of this article). This planning process, including the research outlined above, is expensive in terms of internal and external costs. If you anticipate selling your company for around US$20 million, this process could cost you about 10% of that or US$2 million. But you will have closed your biggest deal ever.

In Part 2, which will appear in CW's November issue: Williams will address the final three stages of the five-step process.

.jpg;maxWidth=300;quality=90;format=webp)

Related Content

Vertical Aerospace eVTOL prototype goes down during uncrewed test flight

The U.K. company has confirmed the Aug. 9 accident that resulted in significant aircraft damage and potential setbacks.

Read More

Composites opportunities in eVTOLs

As eVTOL OEMs seek to advance program certification, production scale-up and lightweighting, AAM’s penetration into the composites market is moving on an upward trajectory.

Read More

Infinite Composites: Type V tanks for space, hydrogen, automotive and more

After a decade of proving its linerless, weight-saving composite tanks with NASA and more than 30 aerospace companies, this CryoSphere pioneer is scaling for growth in commercial space and sustainable transportation on Earth.

Read More

Materials & Processes: Fibers for composites

The structural properties of composite materials are derived primarily from the fiber reinforcement. Fiber types, their manufacture, their uses and the end-market applications in which they find most use are described.

Read MoreRead Next

From the CW Archives: The tale of the thermoplastic cryotank

In 2006, guest columnist Bob Hartunian related the story of his efforts two decades prior, while at McDonnell Douglas, to develop a thermoplastic composite crytank for hydrogen storage. He learned a lot of lessons.

Read More

CW’s 2024 Top Shops survey offers new approach to benchmarking

Respondents that complete the survey by April 30, 2024, have the chance to be recognized as an honoree.

Read More

Composites end markets: Energy (2024)

Composites are used widely in oil/gas, wind and other renewable energy applications. Despite market challenges, growth potential and innovation for composites continue.

Read More