Aerospace growth climbs with carbon fiber

The business case for carbon fiber in narrowbodies has become a lot stronger now that these operational benefits are in evidence.

Adrian Williams is co-founder and managing director of Future Materials Group (Cambridge, UK), an independent strategic advisory firm. Its services include growth strategies, mergers and acquisitions, strategic partnerships and growth capital.

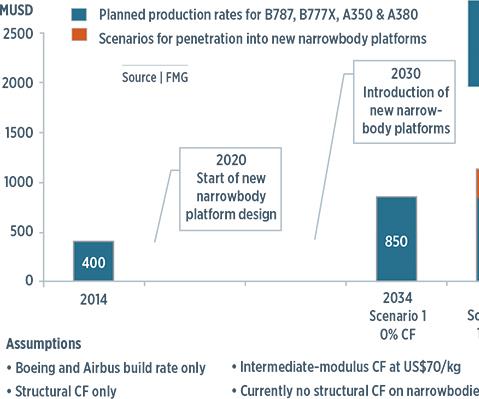

Four possible scenarios for carbon fiber use in narrowbody commercial aircraft range from no structural carbon composites (a highly unlikely Scenario 1), in which widebody production would nevertheless double the carbon fiber market in the next two decades, to Boeing 787-like 50% carbon composite primary structures in narrowbodies (Scenario 4), which would require that a new carbon fiber production line be built every year until 2034. Source: Future Materials Group

Just 10 years ago, three major suppliers of carbon fiber supplied 70% of the worldwide market. Today, the same three suppliers — Toray Industries Inc., Toho Tenax Inc. and Mitsubishi Rayon Co. Ltd. (MRC), all based in Tokyo, Japan — have a combined market share of 45% (excluding Toray’s recent acquisition of Zoltek Corporation, St. Louis, MO, US), with nearly 20 competitors vying for position. Notably, every player in this burgeoning sector of the composites market can point to massive expansion. Overall, there is now three times the capacity and three times the demand for carbon fiber, compared to 2005.

That growth has been reflected not only in the supply chain’s development but also in its value: Hexcel's share price, for example, in June 2005, stood at US$16.30, but by the same date in 2015, it was US$49.49. Hexcel manufactures everything from carbon fiber to finished aircraft structures, and it is in the aerospace industry that carbon fiber has seen massive increases in usage.

The Boeing Co.’s (Chicago, IL, US) 787 and the Airbus (Toulouse, France) A350 XWB and A380 widebody platforms accelerated composites use in aircraft — exceeding the airlines’ requirements for reduced fuel consumption and emissions, reduced maintenance and longer design life, fewer parts, and reduced tooling and assembly costs. Composite materials also deliver an enhanced passenger experience (by damping engine noise/vibration) and a cabin atmosphere less conducive to dehydration. For large, widebody aircraft, carbon fiber delivers a winning value proposition. Competition, legislation and the uncertainty of fuel pricing created the “perfect storm” necessary for technology adoption.

Over the next 20 years, nearly 9,000 new widebodied aircraft are due for delivery, and they will all use predominantly carbon fiber composites for their primary structures. Narrowbody aircraft orders are increasing in similar fashion, typically at a compound annual growth rate (CAGR) of more than 4%, driven by the growth of air travel in China, the Middle East and other emerging markets. Future Materials Group’s recent in-depth research into the specific opportunities for composites in the widebody and narrowbody commercial aircraft markets has underscored some challenges, but also prompted some intriguing conclusions.

For narrowbody aircraft, it might be assumed that carbon fiber demand would mirror that of the past 10 years and continue the widebody story. Yes, there are drivers for carbon fiber adoption for narrowbodies, but our research reveals that there also are barriers that make carbon fiber use less compelling. Narrowbody aircraft demand much higher build rates — often a problem for composites manufacturing processes — and fuel consumption is much less of a factor on short-haul trips. Plus, parts must be designed and built to specifications similar to those for widebodied aircraft, or damage tolerance, tending to increase laminate thicknesses beyond that needed for purely structural reasons. This increases weight and cost, reducing the benefits of carbon fiber.

Industry projections point to nearly 27,000 new narrowbody aircraft deliveries by 2034. By 2030, many of the Boeing 737 and Airbus A320 planes delivered in the 1980s and 1990s will need replacement. New platform designs are in progress, but the level of carbon fiber use in them is unknown at present.

For the operators, however, our data point to emerging drivers that could radically alter the uptake of carbon fiber technology, and those data are based on the track record of quality and reliability that composites have established over the past 10 years. Boeing’s experience with composite floor beams in the Boeing 777 is a good example: In 565 aircraft, not one composite floor beam has been replaced in more than 10 years of commercial flight service. The Boeing 777 composite tail is 25% larger than the Boeing 767 aluminum tail, and yet the maintenance logs show a savings of more than one-third in labor hours. Similarly, Airbus claims that the high penetration of carbon fiber on the A350 XWB will reduce fatigue and corrosion-related maintenance by 60%.

The business case for carbon fiber in narrowbodies has become a lot stronger now that these operational benefits are in evidence. Metal producers are responding to the carbon fiber threat with new alloys and new technologies. Most of all, they are underlining their established position in the supply chain: The relatively low cost of manufacture, the good recyclability of metals, and the wealth of knowledge about metal properties and performance.

Previously, composites suppliers would not have been able to overcome these claims for metal. Although concerns about carbon fiber recyclability remain, carbon fiber’s enhanced durability can reduce some of the issues. At the design stage, stress analysis, finite element analysis, materials selection and mechanical performance are all fully available for composites. Improved fabrication processes are increasing throughput capacity and, thus, carbon fiber part costs are declining. Most of all, major aerospace producers have many years of closely working with the composites supply chain: The days of early adoption and high risk are over.

It is highly unlikely that carbon fiber will not be adopted for the new narrowbody platforms. The question is, how much? On a Boeing 787, 50% of the aircraft is composite, with 20% aluminum, 15% titanium, 10% steel and 5% other materials. If this mix is replicated in narrowbody aircraft, then by 2034 the total carbon fiber market would be more than US$2 billion annually (Scenario 4 in the chart on p. 6). This would necessitate installation of at least one new carbon fiber production line every year until 2034. In the worst case — no structural carbon fiber in any future narrowbody aircraft (Scenario 1) — growth in widebody production alone would more than double the carbon fiber market in 20 years. We anticipate a three-way battle between the airframe OEMs driving down cost and the carbon fiber suppliers and the metal suppliers fighting for market share. Ultimately, the airlines will be the final arbiter and likely to favor a high penetration of carbon fiber for its maintenance and passenger comfort benefits, pointing to Scenario 4 or, possibly, 3, if fiber/metal laminates are successful in narrowbody fuselages.

In summary, the aerospace market for carbon fiber is predictable, manageable and expanding. Demand comes from a relatively small number of large and highly professional manufacturers with long-term design and production cycles. Further, composite materials are an accepted solution to major lightweighting issues, and composite parts are recognized as robust and durable.

So where are the problems? Any increase in volume results in pricing pressure, and to the inevitable commoditization of carbon fiber. On the fiber supply side, market leaders will have to decide whether to protect market share by building capacity, adding value to processes or products, acquiring competitors — or all three.

In addition, the aircraft manufacturers themselves will see greater competition, especially in the narrowbody market, and will need to differentiate: Airframe suppliers in China and Russia are now emerging and with strong home markets could challenge the Boeing and Airbus dominance. Protecting margins in this environment will be challenging.

But the good news is that the quality and performance of carbon fiber structures will not only deliver reduced lifecycle costs, but also make it impossible for metals to regain their previous market share in aerospace.

.jpg;maxWidth=300;quality=90;format=webp)

Related Content

Carbon fiber in pressure vessels for hydrogen

The emerging H2 economy drives tank development for aircraft, ships and gas transport.

Read More

Novel dry tape for liquid molded composites

MTorres seeks to enable next-gen aircraft and open new markets for composites with low-cost, high-permeability tapes and versatile, high-speed production lines.

Read More

Plant tour: Spirit AeroSystems, Belfast, Northern Ireland, U.K.

Purpose-built facility employs resin transfer infusion (RTI) and assembly technology to manufacture today’s composite A220 wings, and prepares for future new programs and production ramp-ups.

Read More

Materials & Processes: Fabrication methods

There are numerous methods for fabricating composite components. Selection of a method for a particular part, therefore, will depend on the materials, the part design and end-use or application. Here's a guide to selection.

Read MoreRead Next

Composites end markets: Energy (2024)

Composites are used widely in oil/gas, wind and other renewable energy applications. Despite market challenges, growth potential and innovation for composites continue.

Read More

From the CW Archives: The tale of the thermoplastic cryotank

In 2006, guest columnist Bob Hartunian related the story of his efforts two decades prior, while at McDonnell Douglas, to develop a thermoplastic composite crytank for hydrogen storage. He learned a lot of lessons.

Read More

CW’s 2024 Top Shops survey offers new approach to benchmarking

Respondents that complete the survey by April 30, 2024, have the chance to be recognized as an honoree.

Read More